Davis Law Group Receives Seattle Business Magazine’s ‘Best Companies to Work For’ Award Learn More

Davis Law Group Receives Seattle Business Magazine’s ‘Best Companies to Work For’ Award Learn More

Personal Injury Protection (PIP) coverage is an extension of car insurance that covers medical expenses and, in many cases, lost wages. PIP is “no-fault” coverage, as it applies and pays out claims regardless of who is at fault.

If you have PIP insurance and are hurt in accident, you can receive maximum benefits whether or not the accident was your fault. On top of medical bills and lost wages, PIP insurance can also cover expenses like transportation to medical appointments.

Washington state law does not require that policy holders obtain PIP insurance coverage. But insurance providers are required by law to offer PIP insurance coverage to their customers. Policy holders can opt out of PIP insurance coverage in writing. If the insurance provider does not obtain a written rejection authorization from the policy holder, then they must add the coverage to the insurance policy.

In Washington state, PIP insurance coverage must, at minimum, provide the following benefits:

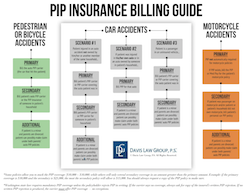

If patient was injured in an auto accident not owned by him/her or another member of the same household…

If patient was injured in his/her own auto or in an auto owned by someone in patient’s household…

If patient was a passenger in an uninsured vehicle…

There are several rules that govern under what circumstances a car insurance company can deny or limit a PIP insurance medical claim.

First, in every case prior to denying a claim for PIP insurance benefits, the insurance carrier must provide the claimant with a written explanation of coverage under the policy, and include a notice that the carrier may deny, limit or terminate benefits in certain situations.

Second, the PIP insurance carrier may only deny, limit or terminate PIP benefits if the treatment is considered either (1) not reasonable, (2) not necessary, (3) not related to the accident, or (4) not incurred within 3 years after the accident. These are the only reasons which will justify a denial of the claim. Only one of these four reasons need be present to justify a denial.

Third, the PIP insurance carrier’s decision to deny, limit, or terminate the claimant’s PIP benefits must be based on the review and opinion of a medical or healthcare professional, i.e., a physician. Specifically, a “medical or health care professional” cannot include an insurance company’s claim representatives, adjusters, or managers or any health care professional in the direct employ of the insurer. Thus, an adjustor cannot deny a PIP claim on his or her own, and without the support of a medical opinion.

Fourth, the medical or healthcare professional relied on by the carrier must be currently licensed, certified, or registered to practice in the same health field or specialty as the health care professional that treated the insured. care professional that treated the insured.

Fifth, if the claimant is being treated by more than one health care professional, the review shall be completed by a professional licensed, shall certified, or registered to practice in the same health field or specialty as the principal prescribing or diagnosing provider, unless otherwise agreed to by the insured and the insurer. This does not prohibit the insurer from providing additional reviews of other categories of professionals.

Finally, the insurance company’s explanation for the denial of PIP insurance benefits must be clear enough so that the claimant does not need to resort to additional research to understand the reason for the action. A simple statement, for example, that the services are “not reasonable or necessary” is not sufficient.

by Davis Law Group Car Accident and Personal Injury Lawyers

★★★★★

Report

IN STOCK (Downloadable)

Price: FREE

Shipping: Downloadable PDF

Get more information on the PIP billing process by downloading our free report. Click below to download.

Report: PDF

Publisher: Davis Law Group Car Accident and Personal Injury Lawyers

Language: English

ID Number: 50-22747213-14

Product Dimensions: 8.5 x 11.0 x 0.3 inches

Shipping: Downloadable PDF

Award-winning attorney Chris Davis has written a series of FREE books about car accident and other personal injury cases in Washington state. These books answer common legal questions that people and their loved ones may have about their legal rights, including how to handle your claim on your own and when you might need an attorney’s help.

Award-winning attorney Chris Davis has written a series of FREE books about car accident and other personal injury cases in Washington state. These books answer common legal questions that people and their loved ones may have about their legal rights, including how to handle your claim on your own and when you might need an attorney’s help.

Get your complimentary copy of “The Ten Biggest Mistakes That Can Wreck Your Washington Accident Case” absolutely free by clicking the “Order Now” button below.

The Washington Accident Books™ is a collection of books, reports, and other materials designed to educate the public about the nature of accidents and the legal rights of injury victims. The Washington Accident Books™ were created as a public service for Washington state residents and is sponsored by award-winning author and attorney Chris Davis of Davis Law Group Car Accident and Personal Injury Lawyers

Complete this CONFIDENTIAL form or call 206-727-4000 for a FREE consultation.